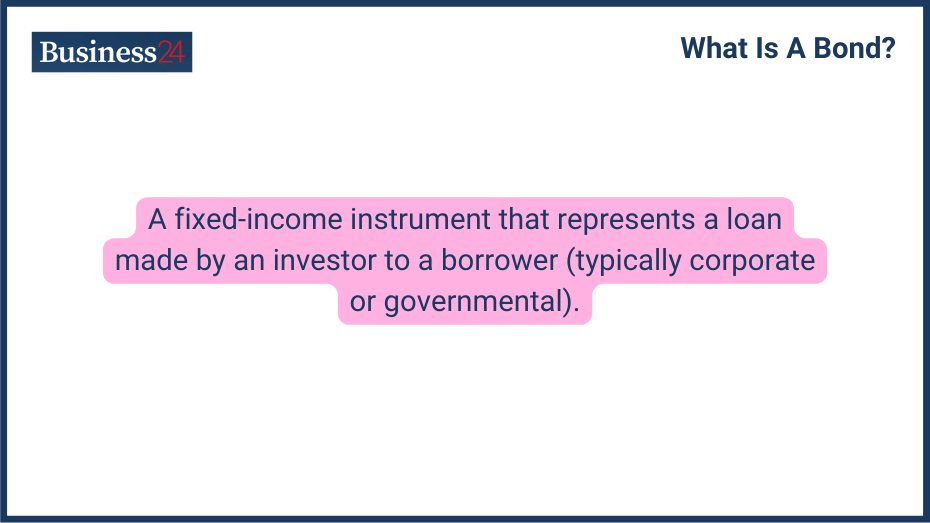

A bond is a fixed-income investment where individuals lend money to a government or company for a specified period at a certain interest rate. The borrower repays the lender with interest along with the bond’s original face value.

Going by definition, we can say a bond is a type of debt security where an investor loans money to an entity they are typically corporate or governmental for a defined period at a fixed interest rate. Bonds are used by companies, municipalities, states, and sovereign governments to finance projects and operations.

When you purchase a bond, you essentially lend your money to the issuer in exchange for periodic interest payments plus the return of the bond’s face value when it matures.

What are the Types of Bonds?

There are various types of bonds issued by different entities and have different characteristics and uses:

Government Bonds

Government Bonds are common and famous bond types. When the government needs money to fund any projects or for any other cause, it issues a bond that you can buy, expecting some interest on your money.

U.S. Treasuries: These include Treasury Bills (T-Bills), Treasury Notes (T-Notes), Treasury Bonds (T-Bonds), and Treasury Inflation-Protected Securities (TIPS).

Municipal Bonds: When a local authority issues a bond, it is known as a municipal bond; these also work for you as tax benefits.

Corporate Bonds

Not only the government but private companies also issue bonds, which companies use to raise capital.

Investment-grade bonds: Investment-grade bonds are safer bonds with low risk and come from good, financially secure companies with high credit ratings.

High-Yield (Junk) Bonds: Opposite to the investment grade bonds these bonds are issued by companies with lower credit ratings while these can offer better interest on your money but carry higher risk.

Other Bonds

As I said, there are different types of bonds that come with different characteristics and uses:

Agency Bonds: Agency bonds are also considered safer bonds issued by the government. Backed companies like Fannie Mae or Freddie Mac these bonds are generally considered safe but may offer slightly lower yields than corporate bonds.

Foreign Bonds: You can also buy bonds issued by foreign governments or companies, offering exposure to international markets and carrying additional currency risk.

Mortgage-Backed Securities: If you know about the 2008 crisis, you would know about mortgage-backed securities. These bonds offer income streams but with prepayment risk, if homeowners pay off their mortgages early.

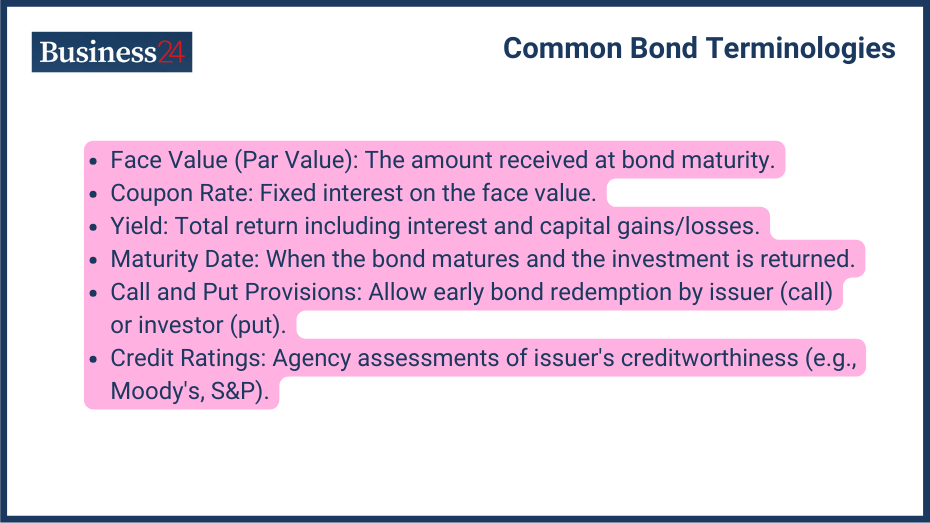

What are Common Bond Terminologies?

It is important to know everything about the investment you are going to make.

Understanding bond terminology is crucial for investors:

- Face Value (Par Value): The amount you will receive when your bond matures is known as face value.

- Coupon Rate: The fixed interest rate paid on the face value.

- Yield: The total return on investment, including interest payments and capital gains or losses you will get on your investment, is known as yield.

- Maturity Date: This is the date when your bond completes the time, and you can get the investment amount.

- Call and Put Provisions: Allow the issuer (call) or the investor (put) to redeem the bond early under specific circumstances.

- Credit Ratings: Assessments by agencies (e.g., Moody’s, S&P) reflecting the issuer’s creditworthiness.

How Exactly Does a Bond Work?

Bonds follow a simple working from issuance to maturity.

Bonds work through the following process:

- Issuance and Pricing: The process starts when a government or corporation needs capital; it issues bonds. These bonds are initially sold at their face value, the principal amount you will receive back when the bond matures. However, the market price of a bond can fluctuate throughout its lifetime.

The price of bonds is mostly influenced by the interest rates because when interest rates increase, bonds become less attractive to investors and the price falls and vice versa.

- Interest Payments: If you want regular income, you can go for bonds. One of the key benefits of the bond is that owning a bond provides a regular stream of income. You will receive periodic interest payments, typically semi-annually. The interest payment amount is calculated by multiplying the bond’s coupon rate by its face value.

For example, if you hold a $1,000 bond with a 5% coupon rate, you will receive $25 in interest every six months until the bond matures.

- Market Price and Interest Rate Relationship: If you want to invest in bonds consider these points as one of the most important. Bond price and interest rates move inversely; if the rates go up, bond prices go down and vice versa.

- Factors Affecting Bond Prices: Other than interest rates, several other factors can influence the market price of a bond. One of the important points to consider is the creditworthiness of the issuer.

Also, I would like to buy bonds that carry low risk. So, Government bonds with a strong past of repaying their debts are generally considered safer and may trade at a higher value.

Likewise, the bonds that have a higher risk of default will trade at a lower price than bonds with lower risk. Also, like any other asset, economic conditions affect the bond price.

What are Investment Strategies with Bonds?

Investors use various strategies to optimize returns and manage risks:

Buy and Hold: If you are investing in bonds, you may be someone who wants lower risk. So, what you can do is buy the bond and hold it until it matures and receive the face value. However, with this strategy, you can miss other opportunities to reinvest your interest payments, which can pay higher interest rates.

Laddering Strategy: If you dont want economic changes to affect your investment, you can choose the laddering strategy. It helps in controlling risk. Investors build a bond ladder by purchasing bonds with staggered maturity dates.

You can buy a portfolio of bonds maturing in one, three, five, and seven years. This way, a portion of your bond portfolio matures each year, providing you with regular access to your principal and allowing you to reinvest it potentially at other opportunities.

Barbell Strategy: By focusing on both short-term and long-term bonds, you can balance your investment with barbell strategy. You get some stability and predictable income from short-term bonds, while long-term bonds offer the possibility of higher returns to grow your investment.

Bond Swapping: You can swap your bond for better interest rates, sell an existing bond, and reinvest the proceeds into a new bond that offers a more attractive yield or better aligns with your current risk tolerance.

What are the Risk Factors in Bond Investing?

Investing in bonds involves several risks:

Interest Rate Risk: As we discussed earlier, the relationship between interest rate and bond price is inverse. Whenever interest rates increase, the price of bonds decreases in value and vice versa.

Credit Risk: Not everyone’s creditworthiness is the same; this is also true for bond issuers. Bonds issued by the US government are considered highly creditworthy but there are bonds that are junk and can lead to loss of capital also.

Inflation Risk: It is true that bonds provide a fixed income, but if the inflation rises, those returns may seem small, and maybe over time, inflation can eat away at the purchasing power of your bond’s interest payments and principal amount.

Reinvestment Risk: As a bond matures, you receive the principal amount and may need to reinvest it. But what if interest rates have fallen since you purchased the bond? Reinvestment risk refers to the challenge of finding new investments with yields that match or exceed your previous one.

Liquidity Risk: Not all bonds are traded actively. Some may be less liquid, meaning it could be difficult to sell them quickly at a fair price if you need the cash.

What are Bond Yields and the Yield Curve?

Understanding bond yields and the yield curve is essential for investors

A bond’s yield reflects the total return an investor can expect if they hold the bond until maturity. It considers the coupon rate (the stated interest) and any capital gains or losses from price fluctuations.

Types of Yield Curve:

The yield curve depicts the relationship between bond maturities and their yields. A normal yield curve slopes upward, indicating higher yields for longer-term bonds. This reflects the inherent risk of locking your money up longer. An inverted yield curve, where short-term yields are higher than long-term ones, can signal a potential economic slowdown. A flat yield curve suggests a more uncertain economic outlook.

The yield curve is an important tool for investors with which you can understand economic conditions and interest rates. An upward curve indicates a healthy economy with growth potential, while an inverted curve can be a warning sign of a recession. Investors can make more informed decisions about their bond allocations by analyzing the yield curve.

What is the Taxation of Bonds?

The taxation of bonds varies based on the type of bond:

Tax Treatment of Interest Income: Like any other income or capital gain from investment bonds, it is also taxed by the government.

Tax-Exempt Bonds: These are types of bonds exempt from federal income taxes. Municipal bonds are often attractive because their interest is exempt from federal income taxes. This can be a significant benefit for investors in high tax brackets. Remember, though, these bonds typically offer lower yields than taxable bonds.

Capital Gains and Losses: You may face capital gains or losses if you sell a bond before it matures. These gains or losses are then taxed according to your tax bracket.

What is the Difference Between Bonds and Other Investments?

Comparing bonds to other investments helps in portfolio diversification:

Comparing Bonds to Stocks: Stocks offer higher returns than bonds, but you don’t want volatility and price swings. You can go for bonds; the return will be less than stocks, but it is a safer investment option.

Bond Funds and ETFs vs. Individual Bonds: A well-diversified portfolio typically includes a mix of asset classes, including bonds. Bonds can help to offset the volatility of ETFs and provide a cushion during market downturns. They can also be a source of regular income for retirees or

What are Practical Applications and Case Studies?

Real-world examples illustrate the practical use of bonds:

Bonds have been an old instrument for loans and investment purposes, and they play an important role in the economy. They are issued by governments, municipalities, and corporations needing money. They offer a relatively stable investment option compared to stocks. Below are some real-world examples that demonstrate the practical use of bonds.

Case Study: Government Bonds During Economic Stability

In periods of economic stability, U.S. Treasury bonds are considered one of the safest investments. For instance, in the mid-2010s, the U.S. economy experienced steady growth with low inflation.

During this period, U.S. Treasury bonds provided consistent interest payments and retained their value, making them a reliable source of income for conservative investors. The stability of the U.S. government backed these bonds, ensuring low default risk.

What are Some Educational Resources and Tools?

Numerous resources can help deepen your understanding of bonds:

If you can find a lot of knowledge out there, you can learn from it. There are various research papers, books, articles, and more you can check out. Such as “The Bond Book” by Annette Thau and articles from financial news outlets like The Wall Street Journal and Investopedia.

If you want to learn in a structured way, you can opt for online courses. They all might not be good, but some courses out there are great learning sources. Additionally, Calculators and Financial Planning Tools are available free of cost on the internet, with tools like Bloomberg’s Bond Calculator and financial planning software like Quicken helping you analyze potential returns and risks associated with different bond options.

Disclaimer

eToro is a multi-asset platform which offers both investing in stocks and cryptoassets, as well as trading CFDs.

Please note that CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 61% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work, and whether you can afford to take the high risk of losing your money

This communication is intended for information and educational purposes only and should not be considered investment advice or investment recommendation. Past performance is not an indication of future results.

Copy Trading does not amount to investment advice. The value of your investments may go up or down. Your capital is at risk.

Crypto assets are complex and carry a high risk of volatility and loss. Trading or investing in crypto assets may not be suitable for all investors. Take 2 mins to learn more

eToro USA LLC does not offer CFDs and makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication, which has been prepared by our partner utilizing publicly available non-entity specific information about eToro.

Braden Chase is an investor, trading specialist, and former research specialist for Forex.com who helps aspiring investors develop the confidence and habits they need to make an income from the market. Braden has served as a registered commodity futures representative for domestic and internationally-regulated brokerages and has also spoken & moderated numerous forex and finance industry panels across the globe.