Mortgage-backed securities (MBS) are an investment like a bond that consist of a bundle of home loans bought from the banks that issued them.

If you know about the financial crisis of 2008, you would know what mortgage-backed security (MBS) is. There was a huge flaw in Mortgage-backed security and the system surrounding it that led to the financial crisis of 2008. In simple words, mortgage-based security (MBS) is an asset backed by a bundle of home loans bought from the bank that issued them.

Introduction to Mortgage-Backed Securities

A Mortgage-Backed Security (MBS) is an investment that gives you a share in the cash flows from a group of residential mortgages. To create these securities, financial institutions bundle mortgages together and sell them to investors as bonds. MBS is a bond-like product that investors can use to generate regular income derived from the homeowners’ mortgage payments.

Securitizing mortgages turns individual, hard-to-sell mortgages into marketable securities. This way, investors get a chance to invest in a diverse range of assets.

Mortgage-backed securities (MBS) first appeared in the United States in the 1970s to direct funds into the mortgage market and boost homeownership. This innovation transformed the financial industry by creating a secondary market for mortgages. It increased liquidity and helped financial institutions manage their mortgage portfolios more efficiently. Mortgage-backed securities were the medium for the 2007-2008 financial crisis.

What is an example of mortgage-backed securities?

For example, let’s say Adam wants to buy a house costing $300,000 and can pay $60,000 upfront from the money he has to buy the home. He goes to the bank to get a loan, and the bank checks Ben’s credit score due to his good financial condition. With the 20% down payment, the bank easily approves the loan.

Now, the process is easy here because of Mortgage-Backed Securities (MBS). The bank gives Adam the loan and then sells it to government-backed entities like Fannie Mae or Freddie Mac. These entities bundle Adam’s mortgage with others into MBS and sell them to investors. Fannie Mae and Freddie Mac don’t give out mortgages directly; they buy them from banks. This process helps banks free up capital and boost their cash flow.

How do mortgage-backed securities work?

It might seem that the working of a mortgage-backed security is complex, but it is not that complex; here is the breakdown so you can understand the workings of a mortgage-backed security:

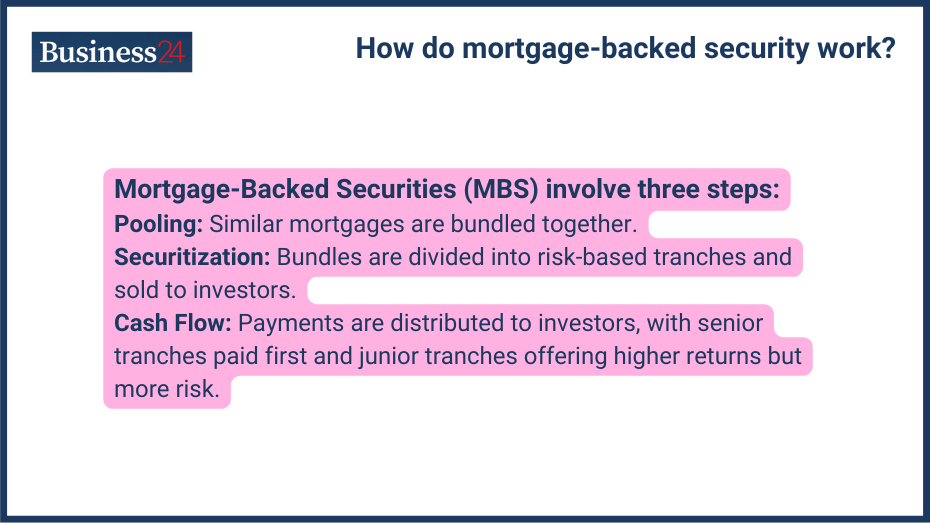

- Pooling of Mortgages: Before the MBS can be represented as an investment option, it needs to pool residential mortgages with similar characteristics like interest rates, loan-to-value ratios, and creditworthiness of borrowers. Now, different mortgages with similar characteristics are pooled together to form a bundle.

- Securitization: Afterwards, according to the different levels of risk and return, these pooled mortgages are divided into different tranches. According to the risk and return factor, they are rated, and then the tranches are sold to investors as securities. Investors who purchase these securities receive periodic payments based on the underlying mortgage payments.

- Cash Flow Distribution: Cash flow from the mortgage pool is distributed to investors according to the tranches’ terms. Investors in senior tranches receive payments first, while those in junior tranches get paid afterward. This setup balances risk and reward: senior tranches offer lower yields with less risk, whereas junior tranches provide higher yields but come with greater risk.

What are the Types of Mortgage-Backed Securities?

Mainly there are two types of mortgage-backed securities:

- Pass-Through Securities

Pass-through securities are the simplest form of MBS in which mortgage payments are collected by the security issuer and passed to the investor. Investors in these securities receive the full amount of principal and interest payments generated by the underlying mortgage pool. These types of securities generally have maturities of 5, 10, 15, or 30 years.

- Collateralized Mortgage Obligations (CMOs)

CMOs are more complex than pass-through securities. In collateralized mortgage obligations, different tranches of securities with varying levels of risk and maturity are created. This allows investors to choose securities that match their risk tolerance and investment horizon. Because every investor has a different capital, time horizon, and risk tolerance. CMOs offer greater flexibility in terms of cash flow and interest rate risk management compared to pass-through securities.

What is the Structure of Mortgage-Backed Securities?

Mortgage-backed securities (MBS) are structured in a way that allows for the distribution of cash flows from the underlying mortgage pool to investors:

Pooling of Mortgages

The pooling process helps to diversify the risk associated with individual mortgages. Thus, the pooling of residential mortgages is the foundation of an MBS. Banks and other institutions gather many of these mortgage loans into one group. The loans in this group usually have similar features, like interest rates and maturity dates.

Tranches and Credit Ratings

Once the mortgage pool is formed, it is divided into different tranches. Each tranche represents a different level of risk and return, and investors can choose to invest in tranches that align with their risk tolerance and investment objectives.

- Senior Tranches: These tranches have the highest priority for receiving principal and interest payments. They are considered the safest tranches and offer lower yields.

- Junior Tranches: These tranches have lower priority for receiving payments and are exposed to higher credit risk. Consequently, they offer higher yields to compensate for the increased risk.

Credit rating agencies assign ratings to MBS tranches based on their creditworthiness. Higher-rated tranches are considered safer investments, while lower-rated tranches carry higher risk.

What is the Process of Creating an MBS?

Process of creating an MBS:

Origination and Securitization

Financial institutions, such as banks and mortgage companies, originate residential mortgages by lending money to homeowners to purchase properties. After the loan is passed, a group of such mortgage loans with similar characteristics is combined to form a mortgage pool.

The mortgage pool is transferred to a special purpose entity (SPE), which issues MBS to investors. The SPE acts as the issuer of the securities and collects mortgage payments from homeowners.

Role of Financial Institutions

Financial institutions play a crucial role in the creation and distribution of MBS; they work as creator and distributors of mortgages. They originate mortgages, pool them, and sell them to investors. Investment banks often act as intermediaries in the securitization process, structuring the MBS and distributing them to investors.

What is the Role of Government in MBS?

In any economy, the government plays an important role in regulating any loans provided by the financial institutions. They regulate the loan market with Government-Sponsored Enterprises (GSEs) and Regulatory Oversight:

Government-Sponsored Enterprises (GSEs)

Government-sponsored enterprises (GSEs) such as Fannie Mae and Freddie Mac play a crucial role in the MBS market. They purchase mortgages from lenders, securitize them, and guarantee the timely payment of principal and interest to investors. This government backing enhances the creditworthiness of MBS issued by GSEs and makes them more attractive to investors.

Regulatory Oversight

The government helps regulate the MBS market to protect investors and keep the financial system stable. Agencies like the Securities and Exchange Commission (SEC) and the Federal Housing Finance Agency (FHFA) oversee the issuing, trading, and risk management of MBS.

What is the Impact of MBS on Financial Markets?

Every financial asset or debt instrument has a direct relation with the financial markets, and instability in any instrument can hugely affect the financial market. There are several benefits as well as risks associated with the MBS:

Benefits:

- Liquidity: MBS provides liquidity to the mortgage market, allowing lenders to recycle funds and originate new loans. This increases the market’s liquidity and helps pass loansed efficiently.

- Diversification: The introduction of mortgage-backed securities has added to the new investment options. Investors can diversify their portfolios by including MBS, which can reduce overall risk. However, there are some risks associated with MBS which can cause harm to investors in conditions like crisis.

- Income Generation: MBS is a types of investment that generate regular income for investors. Investors are paid by the amount of loan paid by the borrower in the form of interest and principal payments.

Risks:

- Interest Rate Risk: The economy’s inflation and interest rate hugely influence MBS. Mortgage-backed securities are sensitive to interest rate fluctuations due to rate cuts and interest rates. When interest rates rise, the value of existing MBS tends to decline.

- Prepayment Risk: Homeowners often refinance their mortgages to get lower interest rates, which leads to prepayments and reduces the expected cash flows from mortgage-backed securities (MBS).

- Credit Risk: One of the main causes of the 2008 financial crisis was loan defaults. Homeowners can default on their loans and not pay the loan amount for various reasons, which can adversely affect the value of the MBS.

Influence on Interest Rates and Lending

- Interest Rate Sensitivity: When interest rates rise, the value of MBS falls because investors want higher yields for new investments. This inverse relationship means that as borrowing costs increase, the attractiveness of existing lower-yield MBS decreases, prompting investors to shift their money to newer, higher-yield options.

- Mortgage Lending: Securitizing mortgages through MBS has boosted mortgage lending, making homeownership more accessible to more people. By converting individual home loans into tradable securities, lenders can free up capital to issue more loans. This process not only increases the availability of credit but also diversifies the risk associated with mortgage lending across a broader investment base.

- Financial Stability: The MBS market is vital to the financial system. Disruptions in this market, like during the 2008 financial crisis, can have widespread economic consequences. When the value of MBS plummets, it can trigger a chain reaction of financial instability, affecting banks, investors, and homeowners. The health of the MBS market is closely tied to the overall economic health, influencing everything from housing prices to the availability of credit in the broader economy.

What was MBS’s role in the 2008 financial crisis?

The 2008 financial crisis exposed the dangers of mortgage-backed securities (MBS) and highlighted the crucial role of the mortgage market in the economy.

Contributing Factors

- Subprime Lending: Banks and lenders issued many subprime mortgages with very loose lending standards, creating a large number of risky MBS. This practice allowed people with poor credit to get mortgages they couldn’t afford, which eventually led to widespread defaults.

- Credit Rating Inflations: Credit rating agencies gave overly optimistic ratings to many MBS, leading investors to believe these securities were safer than they actually were. This mispricing of risk caused investors to pour money into these high-risk investments without fully understanding the potential for loss.

- Leverage and Risk-Taking: Financial institutions took on excessive leverage and engaged in risky trading strategies involving MBS. This meant they borrowed heavily to invest in these securities, which amplified their losses when the housing market collapsed.

Lessons Learned and Reforms

- Stricter Regulation: In response to the crisis, regulators increased oversight of mortgage lending and securitization. This included implementing stricter rules for issuing mortgages and creating MBS to prevent the reckless practices that led to the crisis.

- Improved Risk Management: Financial institutions have since adopted better risk assessment and management practices. They now conduct more thorough evaluations of the risks associated with MBS and other complex financial products to avoid the pitfalls of the past.

- Transparency: There is now greater transparency in the mortgage market, helping investors better understand the risks associated with MBS. This transparency is intended to prevent the kind of blind investment that contributed to the financial crisis.

- Capital Requirements: Financial institutions are now required to hold more capital to absorb potential losses. These higher capital requirements are designed to make banks more resilient in the face of financial shocks, reducing the likelihood of another crisis.

Are mortgage-backed securities a good investment now?

US agency mortgage-backed securities (MBS) are a great option for fixed-income investors right now. The valuations are low, they provide a solid source of income, and the market’s supply and demand dynamics are favorable. Plus, MBS has the potential to outperform other market segments.

However, the decision to invest is dependent on the individual, based on the investor’s goal and risk tolerance.

What is the Comparison with Other Securities?

Key Differences Between MBS and ABS

| Feature | Mortgage-backed securities (MBS) | Asset-Backed Securities (ABS) |

| Underlying Assets | Residential mortgages | Diverse assets (credit cards, auto loans, etc.) |

| Credit Risk | Generally lower credit risk (especially agency MBS) | Credit risk varies based on underlying assets |

| Liquidity | Can vary, but agency MBS typically have higher liquidity | Liquidity can vary depending on the type of ABS |

Comparison with Corporate Bonds

- Issuer: Corporate bonds are issued by corporations, while a pool of mortgages backs MBS.

- Credit Risk: Corporate bonds typically carry higher credit risk than agency MBS, as a corporation’s creditworthiness is often more volatile than that of a diversified pool of mortgages.

- Liquidity: Corporate bonds generally have higher liquidity than MBS, as they are traded on more active markets.

- Yield: Corporate bonds typically offer higher yields than agency MBS to compensate for the higher credit risk.

Disclaimer

eToro is a multi-asset platform which offers both investing in stocks and cryptoassets, as well as trading CFDs.

Please note that CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 51% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work, and whether you can afford to take the high risk of losing your money

This communication is intended for information and educational purposes only and should not be considered investment advice or investment recommendation. Past performance is not an indication of future results.

Copy Trading does not amount to investment advice. The value of your investments may go up or down. Your capital is at risk.

Don’t invest unless you’re prepared to lose all the money you invest. This is a high-risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more

eToro USA LLC does not offer CFDs and makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication, which has been prepared by our partner utilizing publicly available non-entity specific information about eToro.

Braden Chase is an investor, trading specialist, and former research specialist for Forex.com who helps aspiring investors develop the confidence and habits they need to make an income from the market. Braden has served as a registered commodity futures representative for domestic and internationally-regulated brokerages and has also spoken & moderated numerous forex and finance industry panels across the globe.