A tangible asset is an asset that has a finite, transactional monetary value and usually a physical form.

There are various kinds of assets, and nowadays, introducing new assets like NFTs and premium shoes has made the area more diverse. Based on their physical attributes, assets are of two types: tangible and intangible.

Tangible assets are physical assets that can be touched and felt. Infrastructure, equipment, cash, etc., are examples of tangible assets. Intangible assets are non-physical assets such as patents, trademarks, and goodwill, but tangible assets have a physical embodiment. Tangible assets are important and necessary components of a company’s asset base, contributing to its overall value and financial performance.

Tangible assets are essential for a business’s operations, including the infrastructure, equipment, and facilities necessary for production, service delivery, and revenue generation.

What are examples of tangible assets?

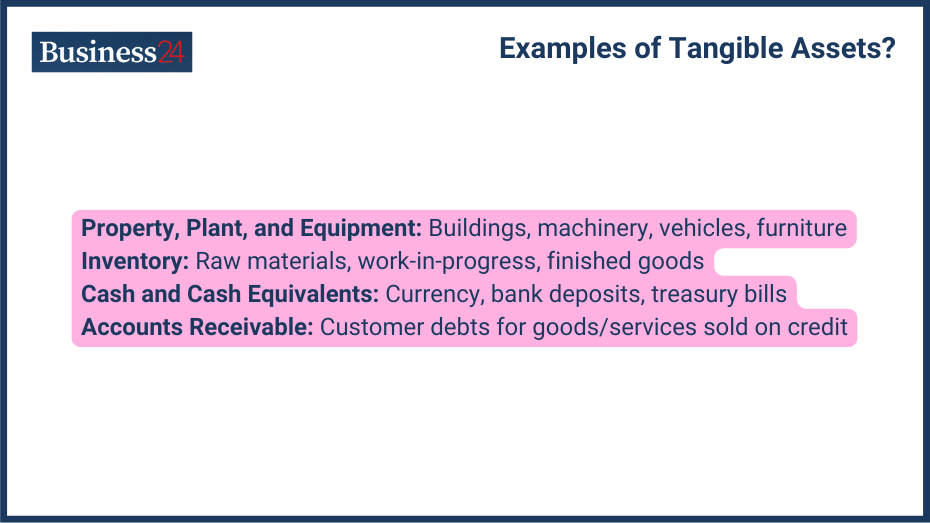

There are various assets that come under the tangible assets, some of which are:

Property, Plant, and Equipment (PP&E):

- Buildings and real estate

- Machinery and equipment

- Vehicles

- Furniture and fixtures

Inventory:

- Raw materials

- Work-in-progress

- Finished goods

Cash and Cash Equivalents:

- Currency

- Bank deposits

- Treasury bills

Accounts Receivable:

- Amounts owed to the company by customers for goods or services sold on credit.

Is cash a tangible asset?

Yes, cash is a tangible asset because it can be touched and felt. It doesn’t have a physical form like a building or machinery but can be exchanged for goods and services. It represents a store of value and is considered a highly liquid asset.

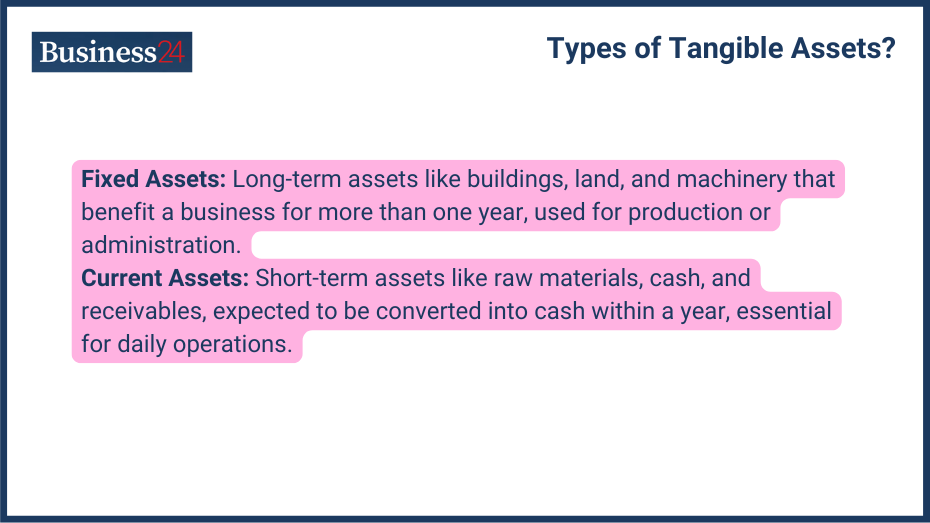

What are the Types of Tangible Assets?

Tangible assets can be categorized broadly into two types:

Fixed Assets

Fixed assets are long-term assets that benefit a business over more than one year. They are typically used to produce goods or services or for administrative purposes. Buildings, lands, machinery, etc., are examples of fixed assets.

Current Assets

Current assets are expected to be converted into cash within one year of the business’s operating cycle. They are essential for day-to-day operations and liquidity. Examples of current assets include raw materials, currency, amount receivables, etc.

What assets are intangible assets?

Intangible assets are those assets that can’t be physically sensed, touched, or felt but can hold value for the owner, like tangible assets. However, they are often considered intellectual property and can significantly value a business. Patents, trademarks, copyrights, and goodwill are examples of intangible assets.

How do you identify tangible assets?

Identifying tangible assets is not a hard thing to do. For those who don’t know, here are some key criteria to identify tangible assets:

- Physical Presence: Assets with a physical presence, such as buildings, machinery, equipment, and inventory, are generally considered tangible assets.

- Usage in Operations: Assets used in the business’s day-to-day operations are tangible assets.

- Measurability: Tangible assets such as land, buildings, and equipment can be measured and quantified.

- Depreciation: Tangible assets are generally subject to depreciation, reflecting their wear and tear over time. Thus, tangible assets subject to wear and tear lose their value over time.

What is the Valuation of Tangible Assets?

Valuing tangible assets is a critical process for financial reporting and decision-making for a business:

Historical Cost

The historical cost method records tangible assets at their original purchase price, including any costs incurred to prepare the asset for use. Over time, tangible assets are depreciated to reflect their wear and tear and decrease in value.

Fair Market Value

Fair market value is the price at which an asset would be sold in an open market between a willing buyer and seller. Various valuation methods, such as comparable sales analysis, cost approach, and income approach, can be used to determine fair market value.

Depreciation Methods

There are various depreciation methods used to evaluate the valuation of tangible assets:

- Straight-Line Depreciation: The straight-line depreciation method allocates the cost of an asset evenly over its useful life.

- Declining Balance Depreciation: This method gives a higher portion of the asset’s cost to earlier years and a lower portion to later years.

- Units of Production Depreciation: Allocates the cost of an asset based on its estimated useful life in units of production.

What is the Accounting for Tangible Assets?

- Recording Tangible Assets on Balance Sheet: Tangible assets must be accounted for regularly and carefully because they can impact a company’s balance sheet. Depending on their expected useful life, they are classified as fixed or current. They are generally recorded at their historical cost, including the purchase price and any costs incurred to prepare the asset.

- Asset Capitalization: When buying a tangible asset, businesses must determine whether to capitalize on its cost or expense it immediately. Capitalization involves recording the asset on the balance sheet and recognizing depreciation expense over its useful life.

- Depreciation Reporting and Compliance: Depreciation allocates a tangible asset’s cost over its useful life. It reflects the asset’s wear and tear, obsolescence, and economic usage. Depreciation expense is recognized on the income statement, reducing the asset’s value on the balance sheet.

- Impairment of Tangible Assets: If the carrying value of a tangible asset exceeds its recoverable amount, which is the higher of the asset’s fair value, less costs to sell, and its value in use, the asset is considered impaired. An impairment loss must be recognized on the income statement to reduce the asset’s value to its recoverable amount. Impairment testing is typically performed annually or whenever there is an indication that the asset’s value may have declined.

What is the Management of Tangible Assets?

Management of tangible assets:

- Asset Tracking and Inventory Management: Accurate records of tangible assets are essential for tracking their location, condition, and value. For this, you must create a detailed inventory list, assign unique identification numbers to each asset, and document relevant information such as purchase date, cost, and expected useful life.

Implementing an efficient inventory management system can also help businesses optimize stock levels, prevent shortages or excesses, and reduce inventory storage and handling costs. - Maintenance and Upkeep of Tangible Assets: Regular inspections of tangible assets help identify and address potential maintenance issues before they escalate into more costly repairs or replacements. Implementing preventive maintenance programs can extend the useful life of tangible assets and reduce unexpected downtime. When necessary, timely repairs and replacements should be carried out to maintain their functionality and value.

- Asset Disposal and Write-Offs: When an asset reaches the end of its useful life or becomes obsolete, it may need to be disposed of. This can involve selling, donating, or scrapping it. Proper accounting treatment must be applied for asset write-offs, including recognizing gains or losses.

What is the Financial Analysis of Tangible Assets?

- Impact on Financial Statements: Tangible assets are reported on the balance sheet as part of total assets, as their value can significantly impact a company’s overall financial position. Depreciation expense related to tangible assets is recognized on the income statement, affecting profitability. Also, the purchase and disposal of tangible assets can significantly impact cash flow.

- Key Financial Ratios Involving Tangible Assets

Asset Turnover Ratio: It measures how efficiently a company uses its tangible assets to generate revenue. It is calculated by dividing net sales by average total assets. A higher asset turnover ratio indicates that a company effectively utilizes its assets to generate sales.

Return on Assets (ROA): This ratio measures a company’s profitability. It is calculated by dividing net income by average total assets. A higher ROA indicates that a company generates higher returns on its tangible assets.

What are the Tax Implications of Tangible Assets?

Tangible assets have significant tax implications for businesses and individuals:

Depreciation Deductions

We have discussed this topic extensively in the above sections. Depreciation expense is tax-deductible, reducing taxable income and lowering the overall tax burden. The choice of depreciation method can also impact the timing of tax benefits.

Capital Gains and Losses

The sale of tangible assets can result in capital gains or losses. Capital gains or losses are generally taxed differently than ordinary income. Certain tangible assets, such as business property, may qualify for Section 1231 treatment, which can impact the tax implications of gains or losses.

Tax Benefits of Tangible Asset Investments

Investing in tangible assets through tax-deferred accounts, such as retirement plans, can defer capital gains taxes. Depreciation can provide tax benefits for businesses and individuals investing in tangible assets.

What are the Strategic Considerations for Tangible Assets?

Role in Business Strategy

- Tangible assets can provide a competitive advantage by enhancing efficiency, quality, or customer experience. For example, investing in modern equipment can improve production efficiency and reduce costs.

- Tangible assets can support business growth and scalability. By investing in additional capacity and infrastructure, businesses can expand their operations and meet increased demand.

- Tangible assets can be used as collateral for loans or to generate cash flow during difficult economic times. This can provide financial flexibility and support business operations.

Investment in Tangible Assets

- Businesses must carefully evaluate tangible asset investments’ potential return on investment (ROI). They must consider the costs associated with acquiring, maintaining, and using the asset and the expected benefits and cash flows.

- Conduct a cost-benefit analysis to compare the potential benefits of a tangible asset investment to the associated costs. Consider factors such as increased revenue, cost savings, and improved efficiency.

- Develop a plan for asset replacement to ensure that aging or obsolete tangible assets are replaced promptly. This can help to maintain operational efficiency and avoid disruptions.

Risk Management and Insurance

- Purchase appropriate insurance coverage to protect tangible assets against loss or damage. This can include property insurance, liability insurance, and equipment insurance.

- Assess the value of tangible assets regularly to ensure adequate insurance coverage. Adjust coverage levels as needed to reflect changes in asset values.

- Implement risk management strategies to minimize the risk of loss or damage to tangible assets. This may involve preventive maintenance, safety procedures, and security measures.

FAQs

Q. What is the difference between tangible and intangible assets?

- Tangible assets have a physical presence, while intangible assets are non-physical. Examples of tangible assets include buildings, equipment, and inventory, while intangible assets include patents, trademarks, and goodwill.

Q. How are tangible assets valued?

- Tangible assets are typically valued using historical cost, fair market value, or depreciation methods.

Q. What is the accounting treatment for tangible assets?

- Tangible assets are capitalized on the balance sheet and depreciated over their useful life.

Q. How do tangible assets affect a company’s financial performance?

- Tangible assets can impact a company’s profitability, cash flow, and financial health.

Q. What are the risks associated with tangible assets?

A. Tangible assets can be subject to risks such as damage, obsolescence, and theft.

Myths and Misconceptions

- Tangible assets are always more valuable than intangible assets: While tangible assets can be beneficial, intangible assets such as intellectual property can also contribute significantly to a company’s success.

- All tangible assets depreciate: Some tangible assets, such as land, may not depreciate over time.

- Tangible assets are always easy to sell: The liquidity of tangible assets can vary depending on factors such as market conditions and the specific asset.

Disclaimer

eToro is a multi-asset platform which offers both investing in stocks and cryptoassets, as well as trading CFDs.

Please note that CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 51% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work, and whether you can afford to take the high risk of losing your money

This communication is intended for information and educational purposes only and should not be considered investment advice or investment recommendation. Past performance is not an indication of future results.

Copy Trading does not amount to investment advice. The value of your investments may go up or down. Your capital is at risk.

Don’t invest unless you’re prepared to lose all the money you invest. This is a high-risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more

eToro USA LLC does not offer CFDs and makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication, which has been prepared by our partner utilizing publicly available non-entity specific information about eToro.